South Korea GDP growth forecast 2026

Key Summary: The South Korea GDP growth forecast for 2026 holds steady at 2.0%, anchored by a strong semiconductor export cycle. However, foreign stakeholders must prepare for potential domestic political shifts, as the Democratic Party of Korea (DPK) proposes stringent corporate regulations and antitrust measures. With the Bank of Korea holding base rates at 2.5% and inflation stabilizing at 2.2%, global investors are encouraged to overweight tech exports, secure favorable long-term commercial leases, and lock in current pro-market tax incentives ahead of the 2027 election cycle.

Table of Contents

- 1. Introduction

- 2. Current Situation Analysis: South Korea Antitrust and Political Policy Shifts

- 3. Global Implications: Analyzing the Regulatory Outlook

- 4. Actionable Insights for Global Investors

- 5. Expert Analysis & Macroeconomic Data

- 6. Conclusion & Next Steps

- Frequently Asked Questions (FAQ)

1. Introduction

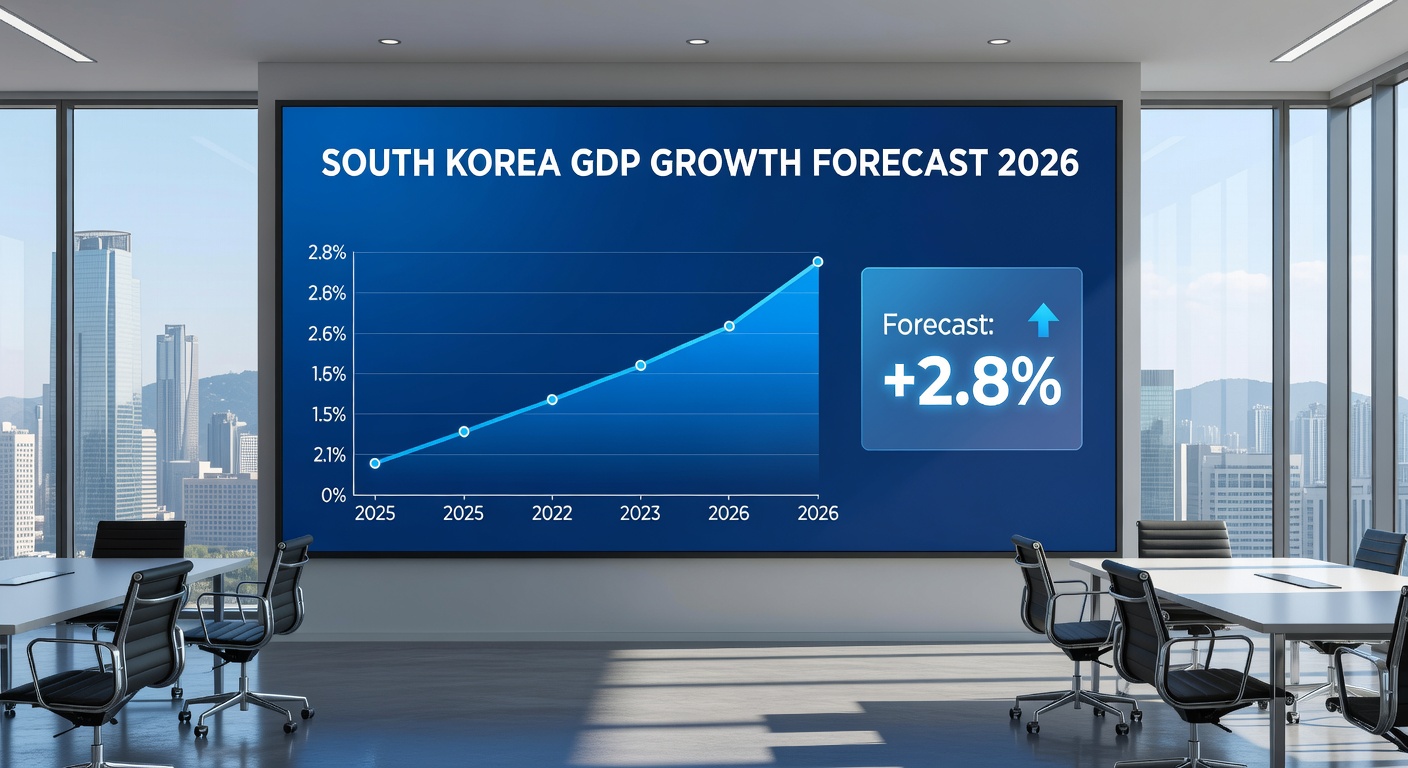

Understanding the South Korea GDP growth forecast 2026 is critical for foreign stakeholders to safeguard capital, especially as potential legislative shifts under the Democratic Party of Korea (DPK) threaten to alter the corporate tax and regulatory environment. As of March 25, 2026, the Bank of Korea has officially revised this vital economic signal to 2.0%. This number is currently grabbing the deep attention of international investors.

South Korea stands as an undeniable powerhouse in global technology supply chains. It is also a foundational pillar of the strong US-Korea security and economic alliance. However, a booming semiconductor export cycle is currently fighting against domestic political winds. For multinational corporations and expats, tracking this shift is highly important to maximize returns in the Indo-Pacific region.

While conservative, market-oriented policies have recently pushed for deregulation and tax cuts, the looming 2027 presidential election cycle is forcing markets to prepare for change.

The market is pricing in new legislative risks. Multinational firms rely on a predictable, free-market business environment to grow. A pivot toward left-leaning populism could disrupt foreign direct investment. It could also heavily alter the landscape of the US-Korea high-tech partnership. Global analysts must begin preparing for these changes today. By looking closely at the data, foreign readers can protect their investments from sudden policy shocks.

There are three key takeaways for investors this year. First, analysts must assess the heavy impact of anti-business regulatory proposals on foreign direct investment. Second, they must evaluate the stable but cautious Bank of Korea interest rate outlook 2026 where rates are held at 2.5%. Finally, investors must navigate the steady South Korea inflation rate projections for investors which hold firm at 2.2%.

Supplemental Explanation: Why Korean Economic Freedom Matters

For global investors and foreign expats living in Seoul, Korean economic freedom is the primary engine of wealth. When conservative market reforms are active, businesses enjoy lower taxes and fewer rules. This allows companies to hire more workers, build new factories, and innovate faster. A free-market approach also strengthens the US-Korea security alliance, as both nations share similar capitalist values.

However, when anti-corporate regulations increase, the cost of doing business goes up quickly. Multinational firms must spend more money on legal compliance instead of research and development. This is why international observers must closely watch the political balance in South Korea. Protecting economic freedom is the best way to ensure long-term growth and stability for both local citizens and global partners.

2. Current Situation Analysis: South Korea Antitrust and Political Policy Shifts

To fully grasp the Korean market, foreign readers must understand two vital concepts. The first is the “Chaebol.” Chaebols are large, family-run business conglomerates like Samsung, Hyundai, and SK. They drive the national economy but currently face heightened antitrust scrutiny from left-leaning lawmakers. The second concept is the “Base Rate.” This is the central bank policy rate that dictates money supply and liquidity. It is the most vital number for the Bank of Korea interest rate outlook 2026.

Right now, despite strong export numbers driven by the semiconductor sector, domestic market health is constrained. The Democratic Party of Korea (DPK) is leveraging its legislative majority to push aggressive corporate oversight bills. Latest 2026 data points paint a very clear picture of the current landscape. Inflation held steady at 2.0% in February 2026. Meanwhile, the KRW to USD exchange rate forecast 2026 anticipates a weaker currency hovering between 1,450 to 1,500 won per dollar.

Despite warnings on rising sovereign debt, recent South Korea sovereign credit rating analysis confirms stability. Fitch holds the nation at AA-, and S&P maintains an AA rating. Leading conservative outlets like Chosun Ilbo and Dong-A Ilbo characterize the DPK’s recent legislative agenda as “anti-business overreach.” They warn that sweeping labor union empowerment and stringent corporate penalties will severely damage national competitiveness. On the other hand, pro-business conservatives continue to push for the expansion of the US-Korea economic alliance through deep deregulation and strict fiscal discipline.

Visual Recommendation: A dual-axis line chart comparing the 2026 won-dollar exchange rate volatility against the central bank base rate holding steady at 2.5%.

| Economic Indicator | 2026 Data / Forecast | Impact on Foreign Investors |

|---|---|---|

| BoK Base Rate | Held at 2.5% | Predictable borrowing costs; supports conservative real estate plays. |

| Inflation Rate | Steady at 2.0% – 2.2% | Protects purchasing power; stabilizes long-term supply contracts. |

| KRW/USD Exchange | 1,450 – 1,500 Won | Boosts tech export profits; increases local operating costs for expats. |

| Credit Rating | S&P (AA), Fitch (AA-) | Signals core market safety despite rising domestic debt warnings. |

Supplemental Explanation: The Battle Over Corporate Regulation

The current situation in South Korea represents a massive clash of economic visions. On one side, conservative policymakers argue that economic freedom is the only sustainable counterweight to an aggressive China. They believe that removing red tape helps South Korean tech giants compete globally. On the other side, left-leaning politicians argue for wealth redistribution and strict chaebol regulation.

For a foreign investor, this political battle translates directly to financial risk. If a company invests heavily in a South Korean subsidiary, new populist labor laws could suddenly restrict their ability to manage their workforce. This explains why conservative media constantly warns against populist excess. Free markets require flexibility, and rigid labor laws scare away smart global money.

3. Global Implications: Analyzing the Regulatory Outlook

The global implications of these economic shifts are massive. A weaker currency, explicitly outlined in the KRW to USD exchange rate forecast 2026, makes South Korean tech exports much more competitive globally. However, this same weak currency increases operating costs for expats and foreign subsidiaries that rely on imported goods.

A potential transition to a DPK-led executive branch raises loud alarms over foreign direct investment risks. Investors worry about increased capital gains taxes, aggressive wealth redistribution policies, and rigid labor market constraints. Historically, these populist policies deter foreign institutional capital from entering the country. Global analysts also worry that a left-leaning administration might adopt a “soft-line” approach toward Beijing. This could heavily complicate US-aligned export controls and force foreign businesses to navigate conflicting geopolitical rules.

When comparing South Korea with global benchmarks, a stark contrast appears. The US and Japan are heavily deregulating to attract tech manufacturing. Meanwhile, the South Korea GDP growth forecast 2026 is buoyed by chip exports but heavily constrained by domestic populist legislative risks. Rising fiscal deficits of over 3% of GDP have been flagged in recent South Korea sovereign credit rating analysis.

This rising debt could trigger massive capital gains tax hikes if left-leaning political factions gain further power ahead of the 2027 election cycle. Foreign tech firms partnering with Korean giants must closely monitor how domestic conglomerates are ramping up compliance. Chaebols are increasing lobbying efforts to insulate their joint ventures from proposed DPK regulatory frameworks. Investors must prepare for a fundamentally adversarial dynamic if the political winds shift leftward.

| Country | Tech Manufacturing Policy | Labor Market Flexibility | Fiscal Approach |

|---|---|---|---|

| United States | Heavy deregulation; massive subsidies. | Highly flexible; pro-business. | Rising debt but global reserve status. |

| Japan | Pro-market reforms; aggressive FDI incentives. | Moderately flexible; improving. | High debt but internally funded. |

| South Korea (Conservative) | Corporate tax cuts; US-alliance focus. | Push for flexibility; pro-growth. | Strict fiscal discipline. |

| South Korea (DPK Threat) | Anti-chaebol penalties; high compliance. | Highly rigid; heavy union power. | Aggressive welfare spending. |

Supplemental Explanation: The Geopolitics of Tech Supply Chains

Foreign businesses do not just look at spreadsheets; they look at maps. The US-Korea security alliance is not just about military defense; it is about protecting vital semiconductor supply chains. When global analysts review the regulatory outlook, they factor in how friendly Seoul is to Washington’s trade goals.

A conservative, market-friendly government aligns perfectly with Western economic freedom. It ensures that critical tech stays out of hostile hands. However, if a populist government takes over, their historically “soft” approach to regional adversaries could create friction. This geopolitical risk is why Fitch recently flagged public finance concerns. For expats and global fund managers, a strong alliance means safe money.

4. Actionable Insights for Global Investors

Institutional investors and expats need specific steps they can take right now. Global readers should leverage the highly predictable Bank of Korea interest rate outlook 2026. Because rates are expected to hold steady at 2.5%, investors can safely hedge their exposure to highly regulated domestic sectors.

It is very wise to avoid domestic utilities and local retail, which are prime targets for populist price controls. Instead, investors should heavily overweight their portfolios with export-driven technology hardware. These sectors remain immune to local consumption slumps and benefit from a weak won. Multinational corporations should conduct immediate stress tests on their Korean subsidiaries. They must quantify the exact compliance costs associated with the antitrust and political policy shifts proposed by the opposition.

Expats and foreign founders must also act quickly. It is highly recommended to accelerate business registrations and real estate acquisitions in Q1 2026. Acting now allows foreign businesses to lock in pro-market tax incentives established under current conservative policies. These favorable rates could vanish before potential legislative reversals target foreign capital.

Furthermore, businesses must factor the steady South Korea inflation rate projections for investors into their daily operations. At 2.2% inflation, long-term commercial real estate leases and supply chain contracts are relatively safe to sign now. For practical help, foreign professionals should access English portals from the Ministry of Economy and Finance (MOEF). They should also use the Bank of Korea Economic Statistics System (ECOS) and Invest Korea tax incentive guides to stay updated on market reforms.

| Target Sector / Area | Recommended Strategy | Reason for Action |

|---|---|---|

| Semiconductors & Tech | Overweight / Buy | Benefits from weak KRW; shielded by US-Korea security pact. |

| Domestic Retail & Utilities | Underweight / Avoid | High risk of DPK price controls and heavy union strikes. |

| Business Registration | Accelerate in Q1 2026 | Lock in conservative pro-market tax breaks before 2027 elections. |

| Commercial Real Estate | Sign Long-Term Leases | BoK interest rates (2.5%) and inflation (2.2%) offer stable pricing now. |

Supplemental Explanation: Locking in Market Reforms

Timing is everything in international business. The market reforms passed by pro-business conservatives have created a golden window for foreign capital. Lower corporate tax rates and eased foreign investment rules make South Korea highly attractive today. However, political landscapes shift.

By accelerating market entry now, expats and global funds can secure legally binding contracts under the current friendly laws. Even if a populist government wins the next election, tearing up existing legal contracts with foreign entities is very difficult. This strategy of moving fast to lock in economic freedom is a classic playbook used by successful multinational firms worldwide.

5. Expert Analysis & Macroeconomic Data

Official forecasts clearly outline the economic reality of the peninsula. Q1 2026 data officially confirms the South Korea GDP growth forecast 2026 is stabilized at 2.0%. However, the IMF strictly warns that aggressive welfare spending could deeply destabilize the long-term debt-to-GDP ratio compared to OECD averages. There is a wide gap between the international perspective and the Korean domestic view.

Domestic media often hyper-focuses on corporate compliance burdens and labor union empowerment. Conversely, international agencies maintaining the South Korea sovereign credit rating analysis look at a bigger picture. They emphasize the massive resilience of the US-Korea tech-security alliance as the ultimate market backstop. This strong alliance provides a safety net that keeps foreign capital from fleeing during domestic political fights.

Expert commentary from conservative think tanks provides deep insight into these risks. The Korea Economic Research Institute (KERI) notes that over-regulation diminishes South Korea’s attractiveness as an alternative base to China for global supply chains. Fitch Ratings also officially notes that “there could be upside to our growth projection for 2026 if global artificial intelligence demand continues.”

Meanwhile, economists at ING Think clearly point out that the central bank sees “no need for immediate tightening as the negative output gap remains.” These expert views confirm that while the export engine is strong, government policy will dictate the final outcome for investors.

Visual Element Recommendation 1: A line graph comparing foreign direct investment (FDI) inflows during periods of conservative deregulation versus periods characterized by heavy DPK-led market intervention.

| Policy Area | Conservative Market Reforms (Current) | Expected DPK Regulatory Outlook (Threat) |

|---|---|---|

| Corporate Taxation | Lower rates to attract global FDI. | Higher capital gains; wealth redistribution. |

| Labor Market | Pushing for flexibility and merit-based pay. | Rigid union empowerment; mandatory profit-sharing. |

| Foreign Policy | Deep US-Korea security and tech alliance. | Soft-line Beijing approach; geopolitical friction. |

| Corporate Governance | Deregulation to boost chaebol exports. | Dismantling holding structures; severe antitrust probes. |

Supplemental Explanation: The Fiscal Danger of Populism

Expert analysis constantly returns to one major fear: public debt. Conservative economists argue that South Korea achieved its miraculous economic growth through hard work, savings, and strict fiscal discipline. If the government shifts toward aggressive welfare spending to satisfy populist demands, the national debt will skyrocket.

Because South Korea has an aging population, borrowing money to pay for welfare is a massive threat to the future economy. Global credit agencies watch this debt-to-GDP ratio very closely. If the country loses its fiscal discipline, its credit rating will drop. This would immediately make borrowing more expensive for every business in the country, choking off economic freedom and innovation.

6. Conclusion & Next Steps

Despite a highly dynamic export sector and a solid 2.0% GDP projection, international stakeholders must rigorously prepare for incoming headwinds. Global readers must prepare for extended currency weakness as the won hovers near 1,500 to the dollar. More importantly, investors cannot ignore the mounting threat of anti-corporate regulatory bloat under potential DPK leadership.

The proposed populist “reforms” frequently mask an anti-corporate agenda that threatens to severely undermine the very free-market dynamism that built modern South Korea. While South Korea remains an incredibly lucrative market, protecting capital requires a proactive, defensive strategy.

Long-term prosperity for foreign capital in Korea ultimately relies on the enduring strength of the US-South Korea alliance. It also relies on a steadfast commitment to economic freedom and regulatory discipline. Institutional funds, multinational corporations, and expats must stay informed and agile. By overweighting tech exports and locking in favorable tax rates now, global investors can successfully ride out any domestic political storms. To dive deeper into these strategies, please explore our related internal content: “Navigating Policy Volatility Under Democratic Party Rule,” “Expats Guide to the 2026 Won-Dollar Exchange Rate,” and “Read our full 2026 report on the US-Korea Security Alliance.”

We highly encourage all international readers to subscribe to our Global Investor Newsletter. Subscribers receive real-time, 100% English-language updates on South Korean corporate regulation, US-alliance developments, and exclusive pro-market macroeconomic analysis.

Updated 2026 Resource List for Global Investors:

- 2026 Policy Papers from the US Chamber of Commerce in Korea (AMCHAM)

- Bank of Korea Q1 2026 Monetary Policy Report

- Fitch Ratings APAC Credit Outlook 2026

- Ministry of Economy and Finance (MOEF) English Directives

- Korea Economic Research Institute (KERI) Market Freedom Index 2026

Supplemental Explanation: Securing Your Financial Future in Korea

Investing in a foreign country always carries unique risks, but knowledge is your best defense. By understanding the distinct differences between conservative market reforms and populist regulation, you can make smarter money choices. South Korea is at a critical crossroads in 2026. The decisions made by lawmakers this year will echo into the 2027 elections and beyond.

For the global expat and the international fund manager, staying aligned with pro-market data is essential. Keep monitoring the central bank rates, watch the export numbers, and always hedge against anti-business legislation. Your financial success in the Indo-Pacific depends on seeing the regulatory threats before they become law.

Frequently Asked Questions (FAQ)

Q: What is the official South Korea GDP growth forecast for 2026?

A: As of March 2026, the Bank of Korea has officially revised the GDP growth projection to 2.0%. This growth is heavily supported by a strong semiconductor export cycle.

Q: How will the potential DPK legislative shifts affect foreign investments?

A: Potential left-leaning populist policies by the Democratic Party of Korea (DPK) pose risks of increased anti-corporate regulations, rigid labor laws, and higher capital gains taxes. This could heavily alter the corporate environment and disrupt foreign direct investment.

Q: What is the 2026 outlook for the Bank of Korea base interest rate?

A: The Bank of Korea is holding the base interest rate stable at 2.5%. This predictability supports conservative real estate plays and helps investors calculate long-term borrowing costs.

Q: Which business sectors should global investors focus on in South Korea right now?

A: Investors are highly encouraged to overweight export-driven technology hardware and semiconductors, which benefit from the current weak won (1,450 to 1,500 per dollar). Conversely, domestic retail and utilities should be avoided due to the threat of populist price controls.